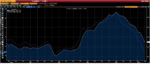

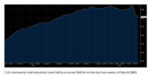

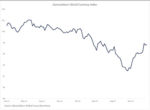

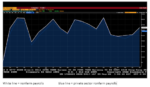

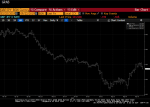

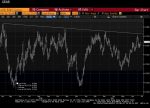

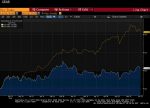

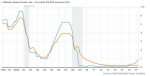

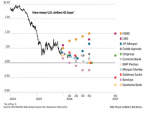

The resilience of the

US economy and stickiness of price pressures spurred a reassessment of the

trajectory of Fed policy. This sparked a sharp rise in US interest rates and

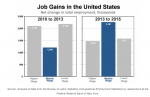

extended the dollar’s advance. The somewhat disappointing April jobs report and

a softer CPI report in the middle of May could signal that the interest rate

adjustment is over. Federal Reserve Chair Powell played down the likelihood of

the need to lift rates again, and as it was in Q4 23, when CPI moderated to a 2%

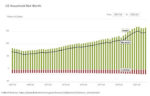

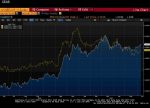

annualized rate, the central bank is being prudent in both directions. The IMF identified US fiscal policy

as a key to fueling demand, inflation, and the stronger greenback, which has

heightened concern among several countries in the Asia Pacific region,

including Japan, South Korea, China, and Indonesia.

2024-05-04

May 2024 Monthly