Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Gold traders on trial: Only buy physical

Gold traders on trial: Only buy physical15 Jul 2022

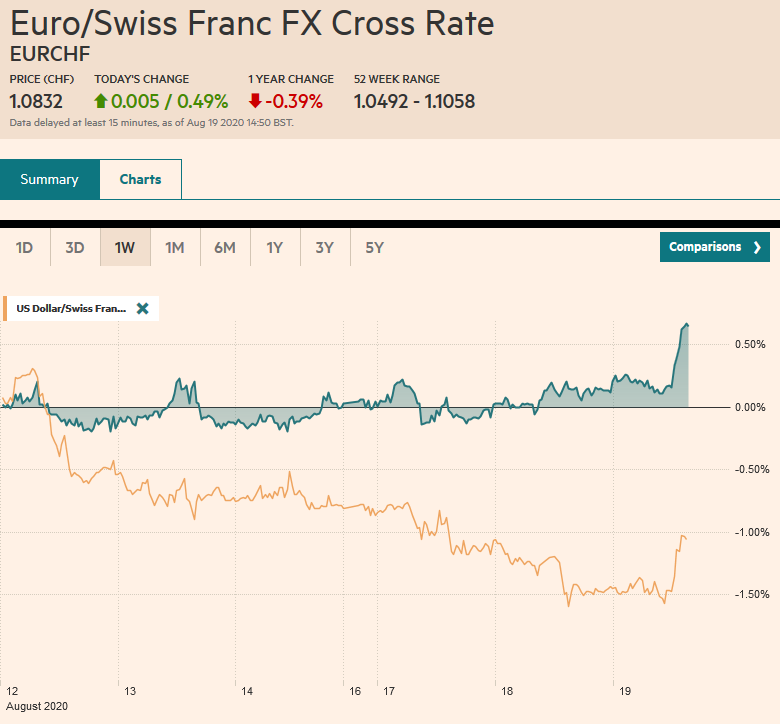

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback19 Aug 2020

FX Daily, July 20: Markets Yawn, Deal or No Deal20 Jul 2020

Cool Video: TD Ameritrade-Stocks, the Dollar and the Trap Laid by the German Court7 May 2020

New Month, New Trends?

New Month, New Trends?5 May 2020

FX Daily, January 29: Escaped from a Crocodile’s Mouth, Entered a Tiger’s Mouth29 Jan 2020

FX Daily, January 7: Geopolitical Angst Eases, Helps Equities and Underpins the Greenback7 Jan 2020

FX Daily, September 25: Risk Appetite Stymied: Dollar Recovers while Stocks Slide25 Sep 2019

FX Daily, August 29: Johnson Faces Legal Challenges and Conte may be Given an Extension29 Aug 2019

FX Daily, August 20: Marking Time Ahead of PMI and Powell20 Aug 2019

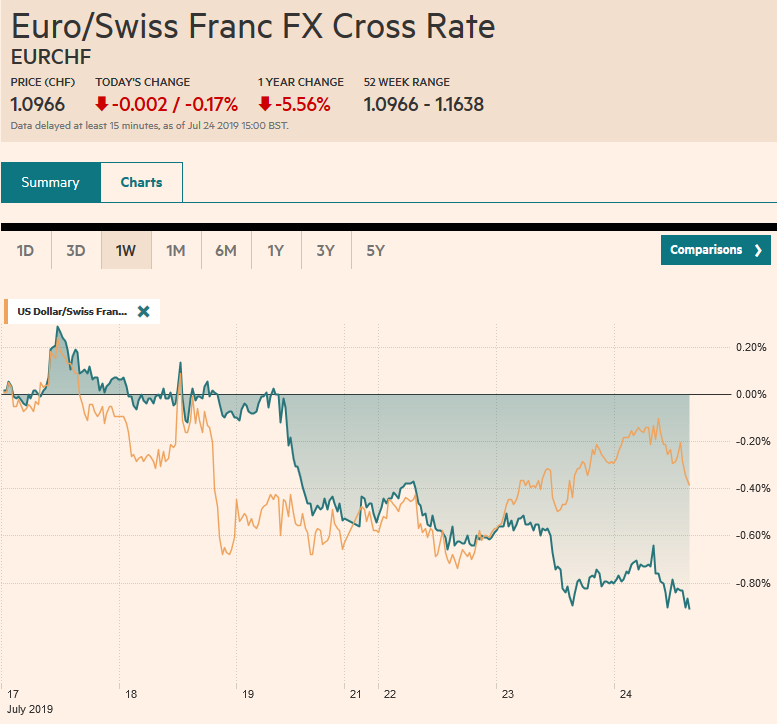

FX Daily, July 24: Poor PMI Weighs on Euro Ahead of ECB24 Jul 2019

Cool Video: End of Tariff Truce Spurs Over Correction21 May 2019

FX Daily, May 10: Waiting for the Other Shoe to Drop10 May 2019

FX Daily, March 26: Semblance of Stability Re-Emerging26 Mar 2019

FX Daily, March 25: Monday Blues: Equities Pare Quarterly Gains25 Mar 2019

FX Daily, March 14: Another UK Vote, but No Closure14 Mar 2019

FX Daily, March 11: Greenback Starts New Week Decidedly Mixed, with Brexit Anxiety Weighing on Sterling11 Mar 2019

FX Weekly Preview: Brexit Comes to a Head, and while Europe and US Data Rebound, the Equity Rally Falters11 Mar 2019

FX Daily, March 08: Equities Slump on Growth Concerns ahead of US Jobs8 Mar 2019

FX Daily, March 07: EMU Looks to ECB7 Mar 2019

Gold traders on trial: Only buy physical

2022-07-15

by Stephen Flood

2022-07-15

Read More »