Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

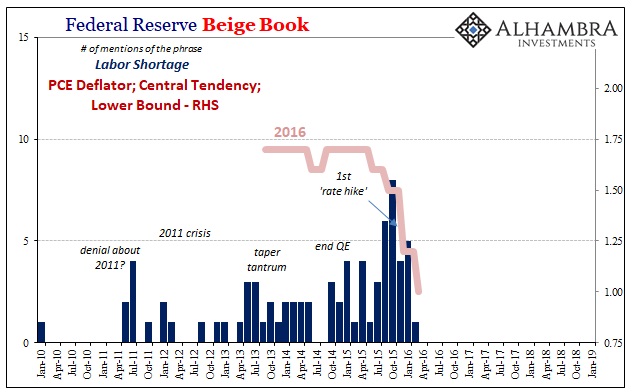

Hall of Mirrors, Where’d The Labor Shortage Go?

Hall of Mirrors, Where’d The Labor Shortage Go?20 Jan 2019

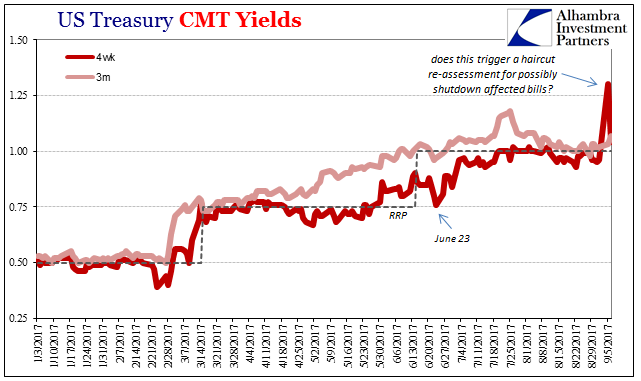

It Was Collateral, Not That We Needed Any More Proof30 Sep 2017

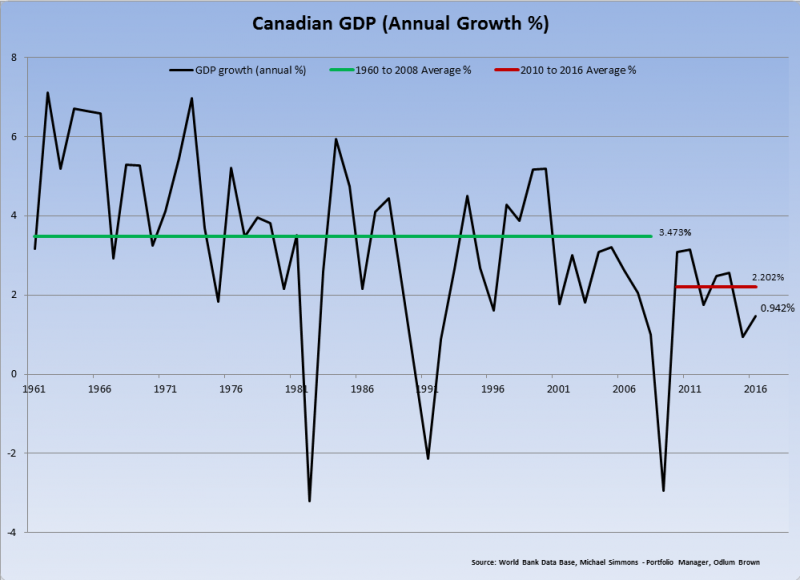

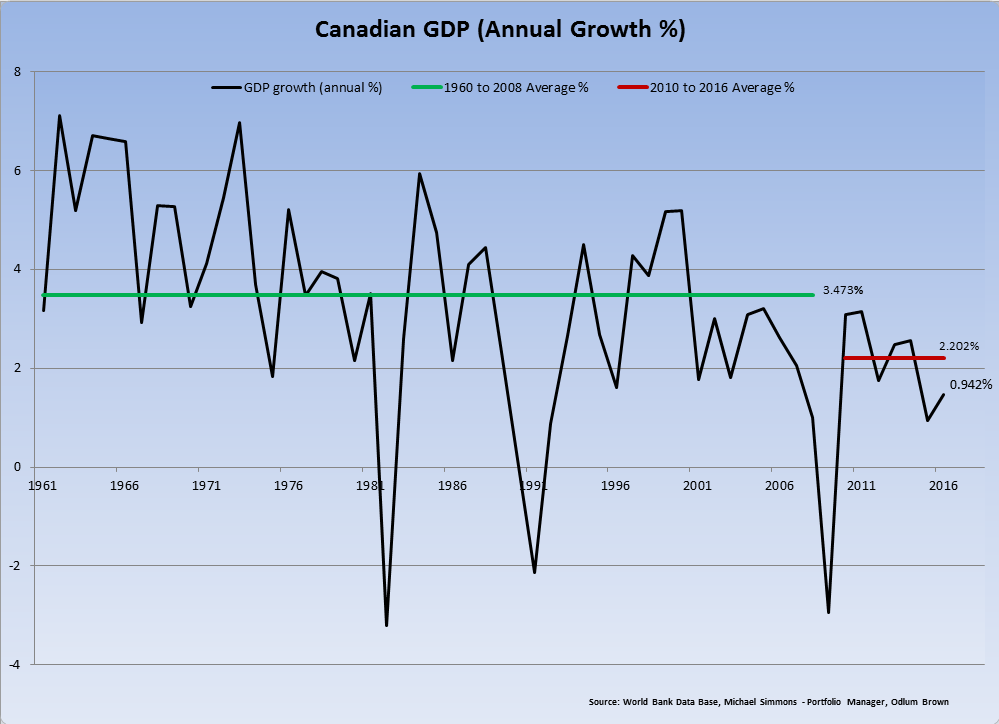

Canada’s RHINO(s)

Canada’s RHINO(s)14 Sep 2017

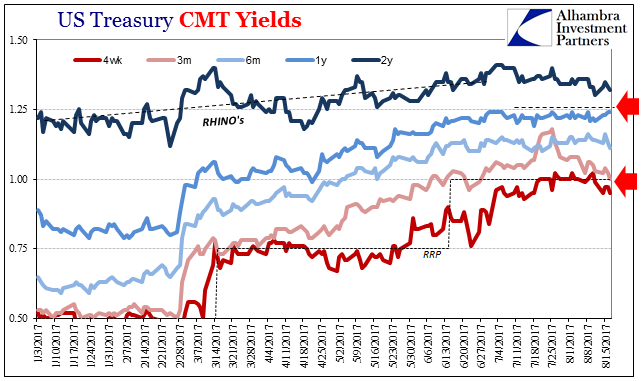

United States: The Fed Tries To Tighten By Rates, But The System Instead Tightens By Repo23 Aug 2017

Data Dependent: Interest Rates Have Nowhere To Go18 Aug 2017

Repeat 2015; An Embarrassing Day For The Fed

Repeat 2015; An Embarrassing Day For The Fed24 Jun 2017