Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Dollar Recovers After Losses Extended in Asia

Dollar Recovers After Losses Extended in Asia29 Nov 2023

Weekly Market Pulse: There Is No Certainty In Investing

Weekly Market Pulse: There Is No Certainty In Investing18 Jul 2022

Market Pulse: Mid-Year Update

Market Pulse: Mid-Year Update24 Jun 2022

“Inflation” Not Inflation, Through The Eyes of Inventory

“Inflation” Not Inflation, Through The Eyes of Inventory11 Jun 2022

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

Can’t Blame COVID For This One

Can’t Blame COVID For This One3 Jun 2022

Shipping Around Retail ‘Inflation’

Shipping Around Retail ‘Inflation’22 May 2022

T-bills Targeted Target

T-bills Targeted Target20 May 2022

Synchronized Not Coronavirus

Synchronized Not Coronavirus19 May 2022

Not Good Goods

Not Good Goods24 Apr 2022

Shanghai’s Current Plight Began in 2017

Shanghai’s Current Plight Began in 201723 Apr 2022

Weekly Market Pulse: The Cure For High Prices

Weekly Market Pulse: The Cure For High Prices31 Mar 2022

Briefing Even More Inventory

Briefing Even More Inventory1 Mar 2022

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data29 Jan 2022

Trying To Project The Goods Trade Cycle

Trying To Project The Goods Trade Cycle17 Dec 2021

Weekly Market Pulse: Time For A Taper Tantrum?

Weekly Market Pulse: Time For A Taper Tantrum?20 Sep 2021

August Retail Sales Surprise To The Upside, Because They Were Down?

August Retail Sales Surprise To The Upside, Because They Were Down?17 Sep 2021

Weekly Market Pulse: Is It Time To Panic Yet?

Weekly Market Pulse: Is It Time To Panic Yet?12 Jul 2021

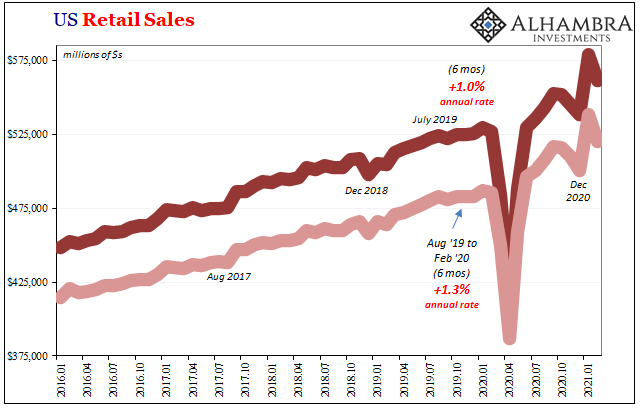

Another Round of Transitory: US Retail Sales & (revised) IP

Another Round of Transitory: US Retail Sales & (revised) IP16 Jun 2021

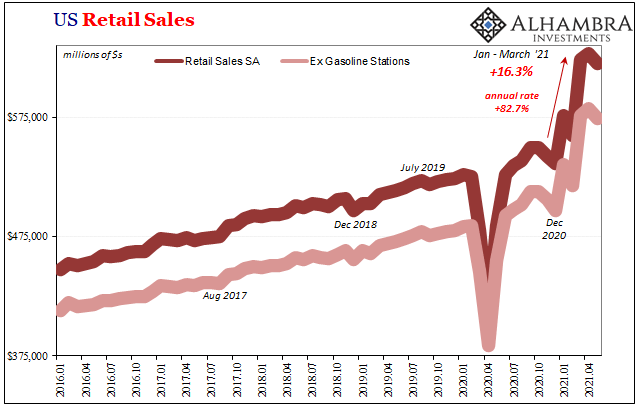

Spending Here, Production There, and What Autos Have To Do With It

Spending Here, Production There, and What Autos Have To Do With It17 Mar 2021