Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

The Biggest Risk, No Surprise, Collateral

The Biggest Risk, No Surprise, Collateral28 Jun 2022

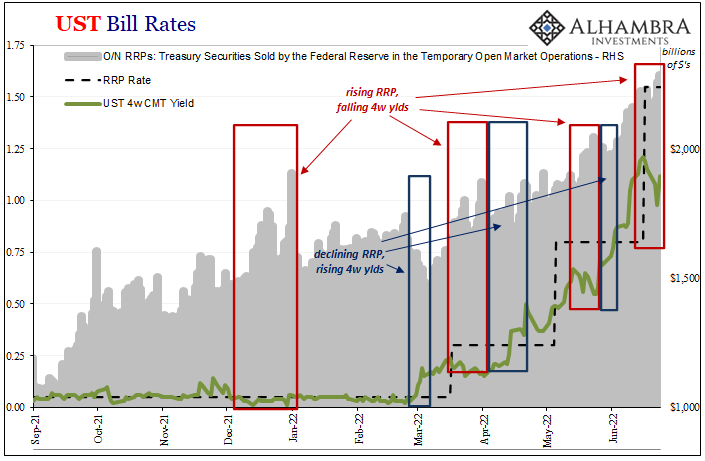

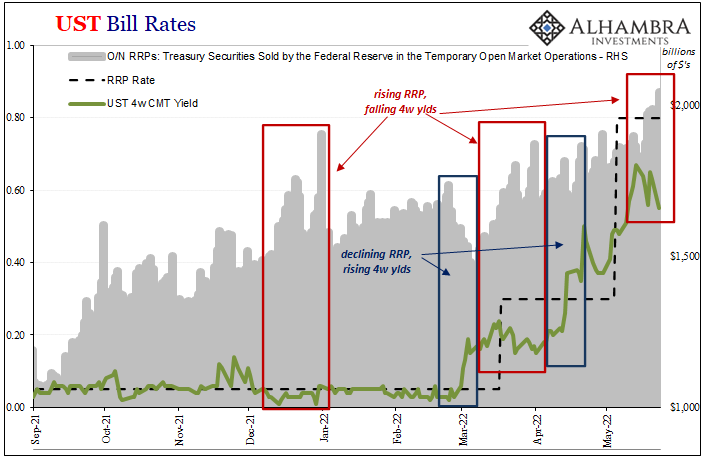

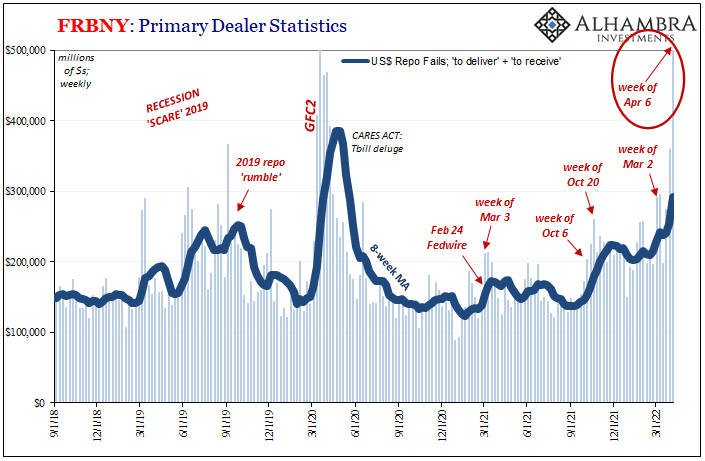

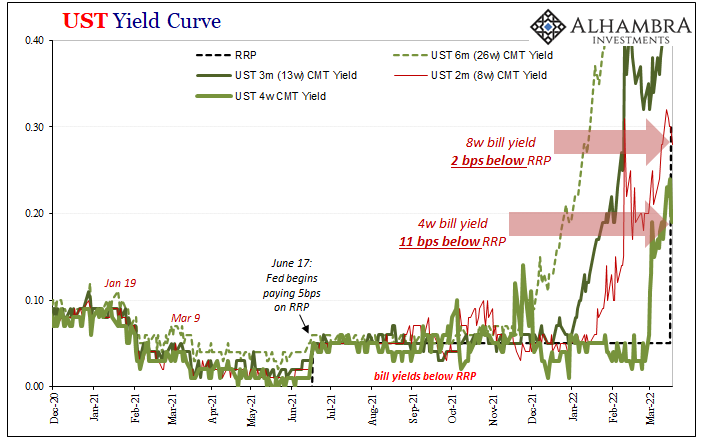

RRP (use) Hits $2T, SOFR Like T-bills Below RRP (rate), What Is (really) Going On?

RRP (use) Hits $2T, SOFR Like T-bills Below RRP (rate), What Is (really) Going On?27 May 2022

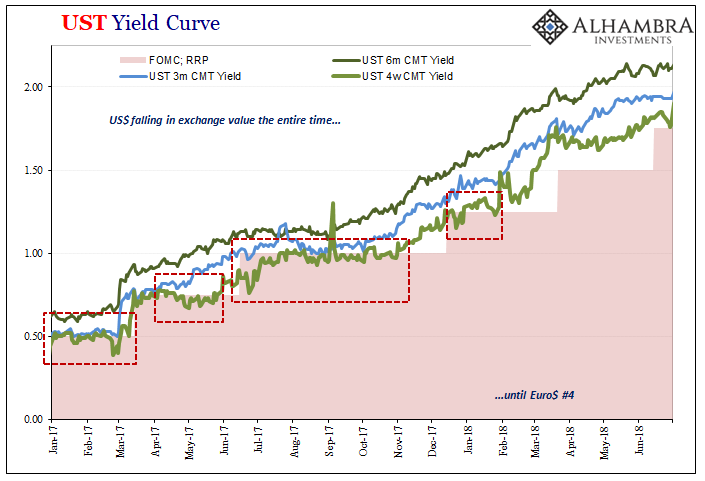

T-bills Targeted Target

T-bills Targeted Target20 May 2022

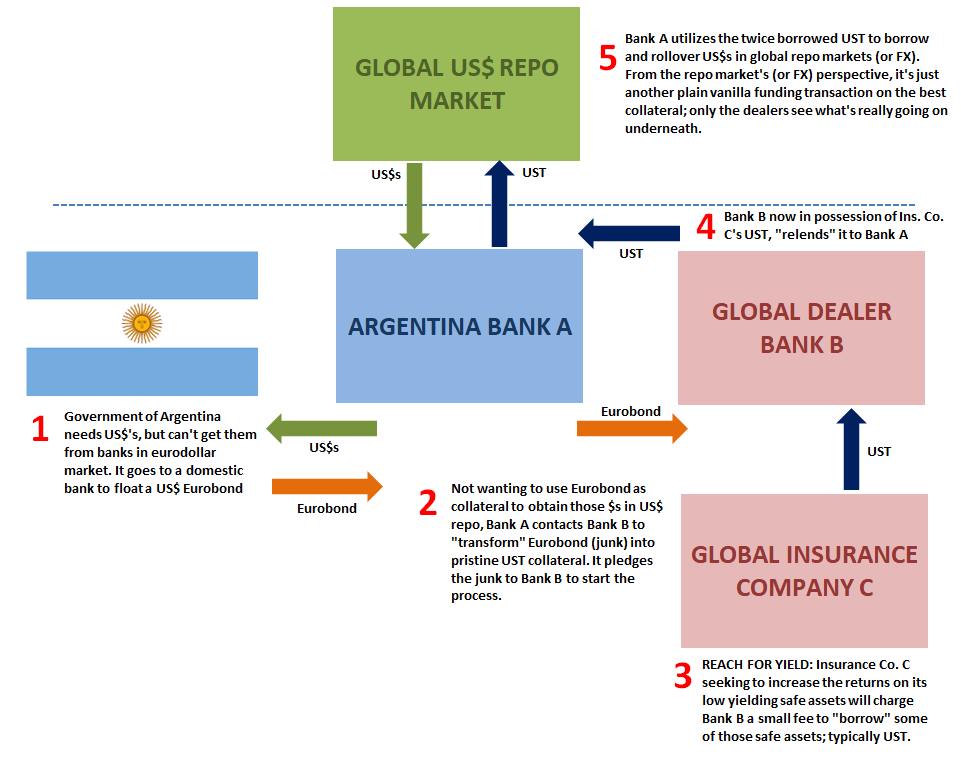

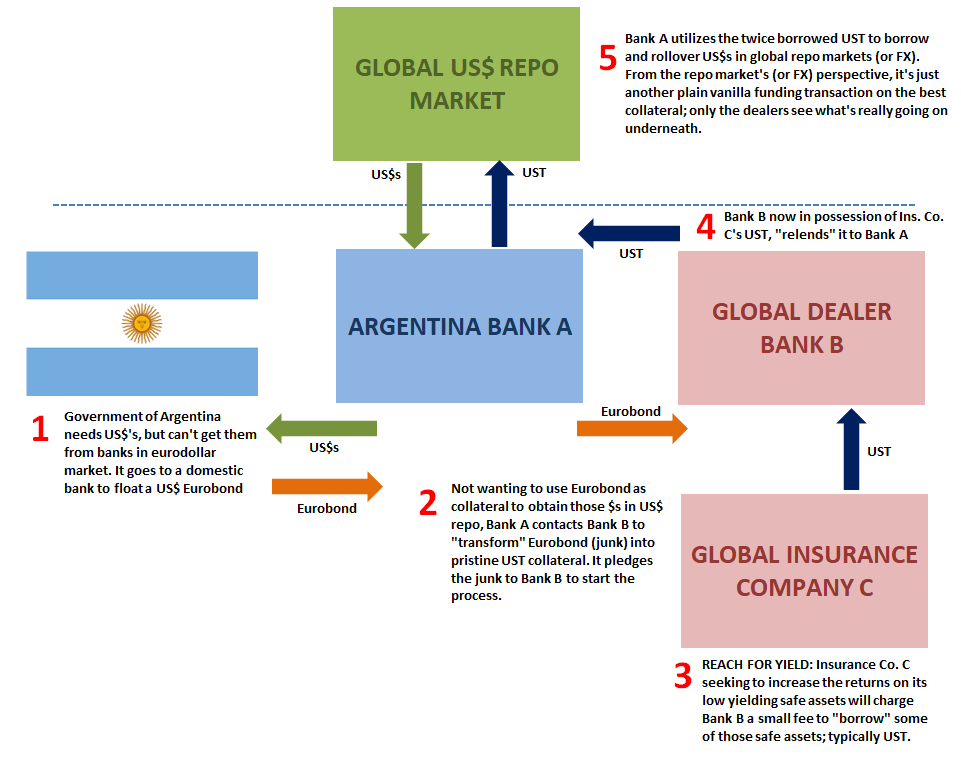

Eurobonds Behind Euro$ #5’s Collateral Case

Eurobonds Behind Euro$ #5’s Collateral Case12 May 2022

Collateral Shortage…From *A* Fed Perspective

Collateral Shortage…From *A* Fed Perspective7 May 2022

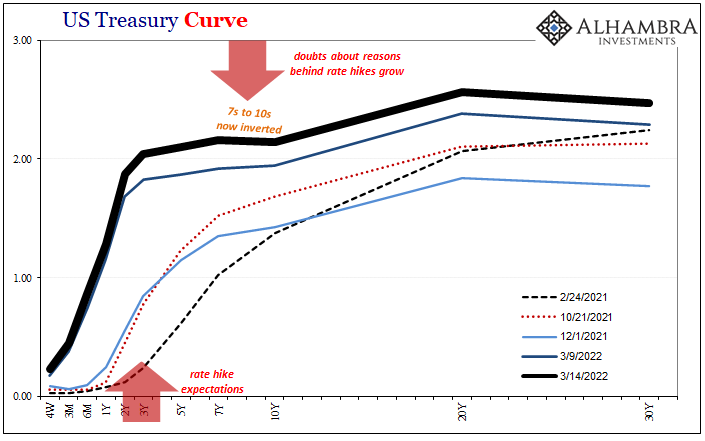

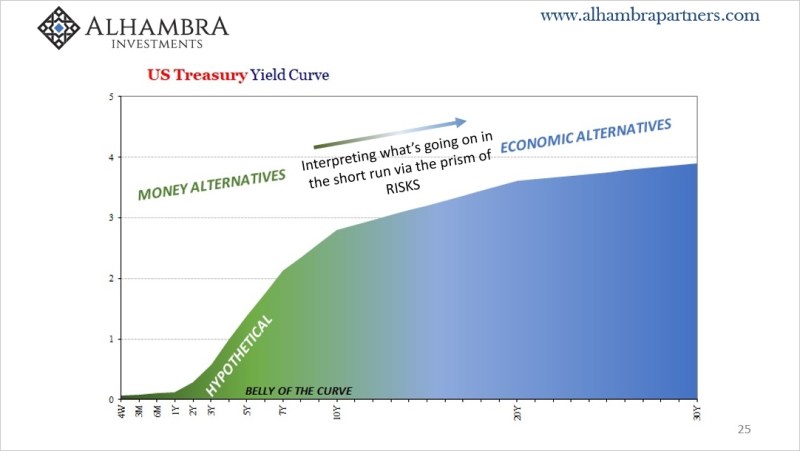

Yield Curve Inversion Was/Is Absolutely All About Collateral

Yield Curve Inversion Was/Is Absolutely All About Collateral18 Apr 2022

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)21 Mar 2022

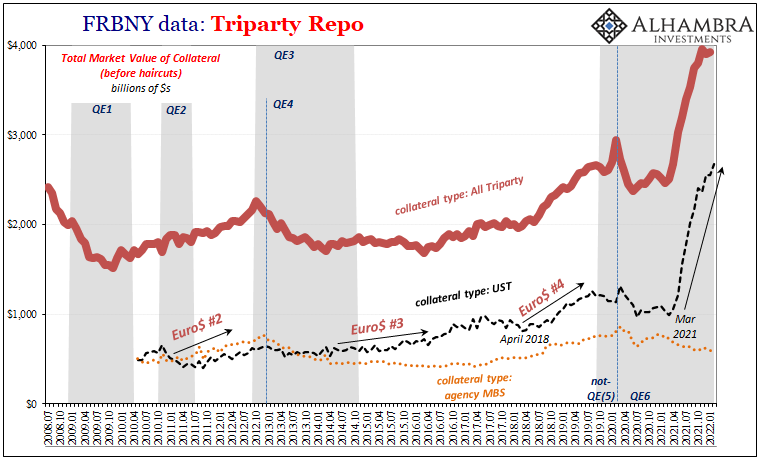

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]18 Mar 2022

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 1]

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 1]17 Mar 2022

So Much Fragile *Cannot* Be Random Deflationary Coincidences

So Much Fragile *Cannot* Be Random Deflationary Coincidences10 Mar 2022

The Curve Is Missing Something Big

The Curve Is Missing Something Big21 Oct 2021

CPI’s At Fives Yet Treasury Auctions

CPI’s At Fives Yet Treasury Auctions12 Aug 2021

Golden Collateral Checking

Golden Collateral Checking27 Jul 2021

Rechecking On Bill And His Newfound Followers

Rechecking On Bill And His Newfound Followers9 Apr 2021

Deja Vu: Treasury Shorts Meet Treasury Shortages

Deja Vu: Treasury Shorts Meet Treasury Shortages10 Mar 2021

For The Dollar, Not How Much But How Long Therefore How Familiar

For The Dollar, Not How Much But How Long Therefore How Familiar24 Feb 2021

What Might Be In *Another* Market-based Yield Curve Twist?

What Might Be In *Another* Market-based Yield Curve Twist?23 Feb 2021

Just Who Is, And Who Is Not, Selling T-Bills

Just Who Is, And Who Is Not, Selling T-Bills29 Nov 2020

Treasury Auctions Are Anything But Sorry Because They’ve Never Been Sorry About Solly

Treasury Auctions Are Anything But Sorry Because They’ve Never Been Sorry About Solly28 Nov 2020

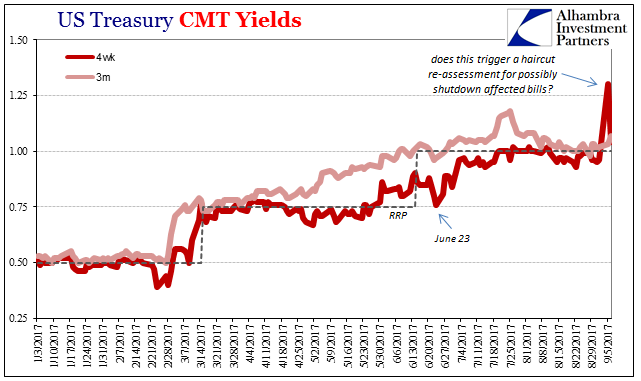

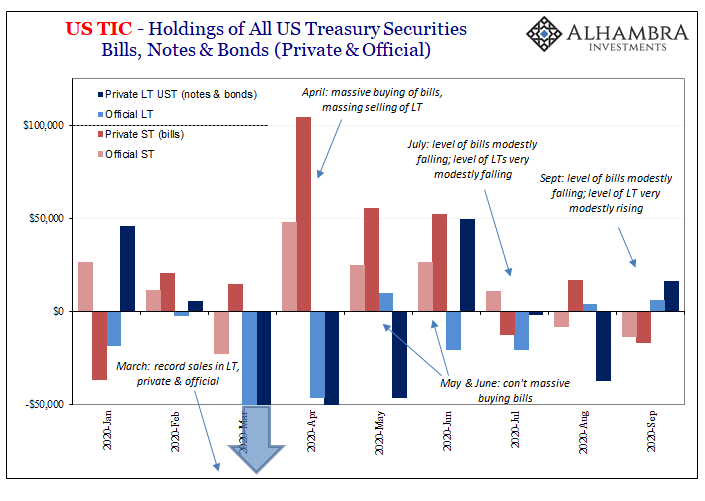

What’s Zambia Got To With It (everything)

What’s Zambia Got To With It (everything)1 Oct 2020