Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

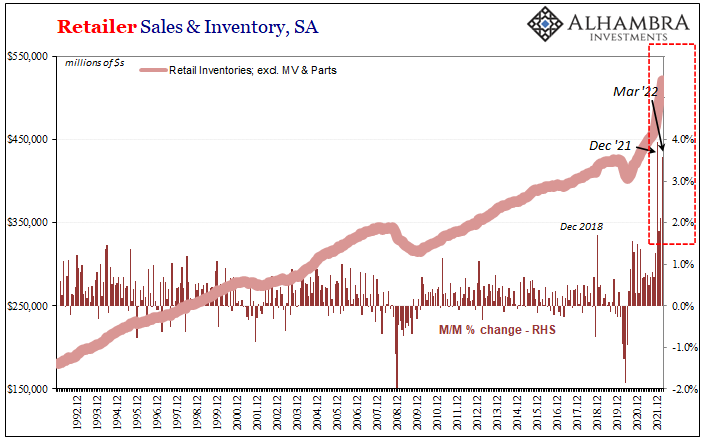

Inventory Flood Continues Just As Consumers Tap Out

Inventory Flood Continues Just As Consumers Tap Out31 May 2022

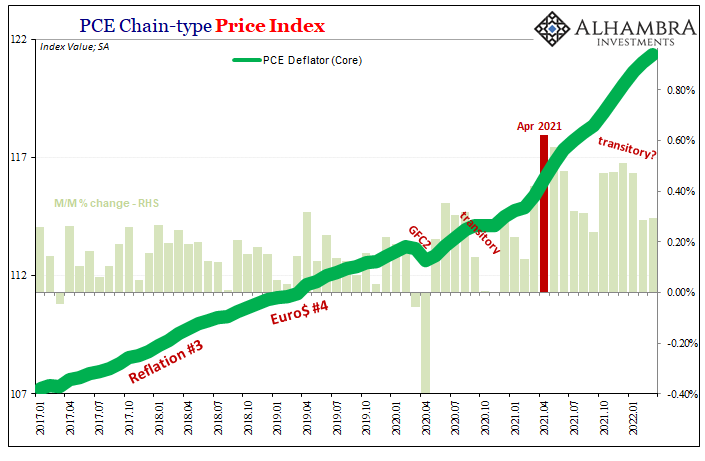

Some ‘Core’ ‘Inflation’ Difference(s)6 May 2022

The Short, Sweet Income Case For Ugly Inversion(s), Too4 Apr 2022

White-Hot Cycles of Silence28 Dec 2021

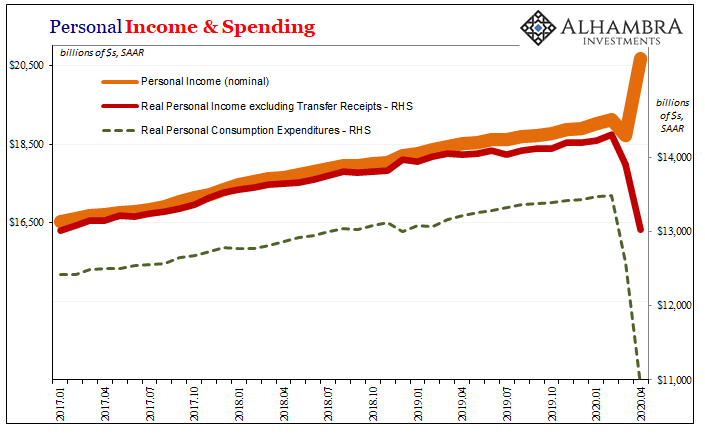

Personal Income and Spending: The Other Side1 Jun 2020

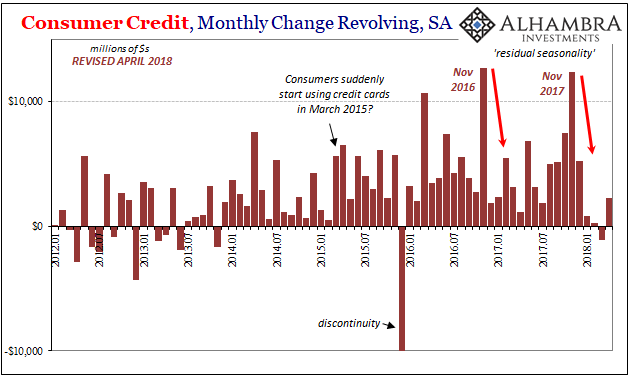

Recent Concerning Consumer Credit Trends Carry On Into April16 Jun 2018

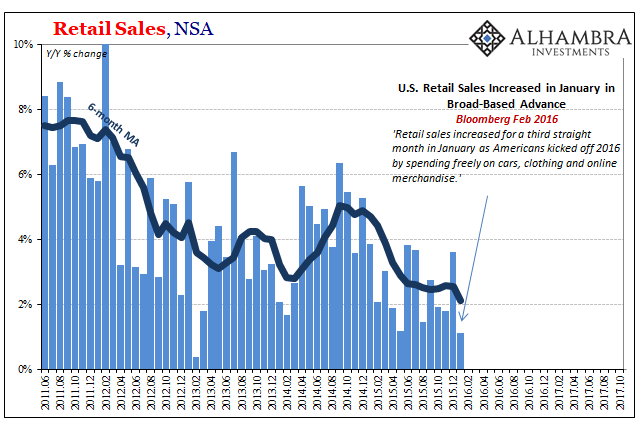

Retail Sales, Consumer Sentiment, And The Aftermath Of Hurricanes

Retail Sales, Consumer Sentiment, And The Aftermath Of Hurricanes17 Jan 2018

The (Economic) Difference Between Stocks and Bonds4 Nov 2017

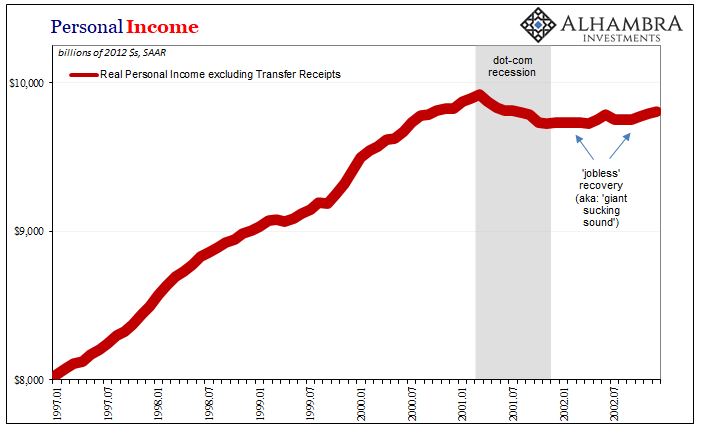

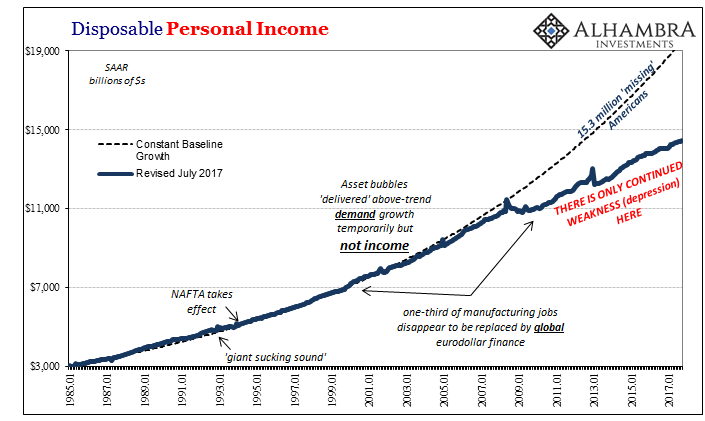

Incomes Are What Matters, So Bad Month, Bad Year, Bad Decade8 Oct 2017

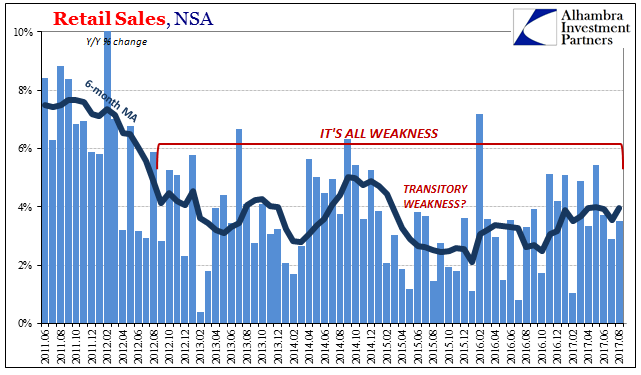

Retail Sales and the End of ‘Reflation’22 Sep 2017

US Export/Import: ‘Something’ Is Still Out There13 Sep 2017

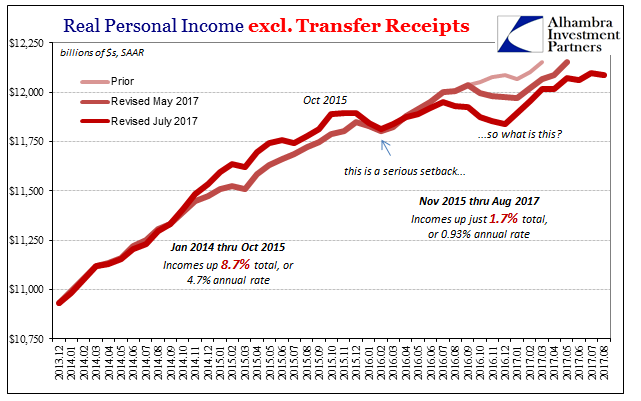

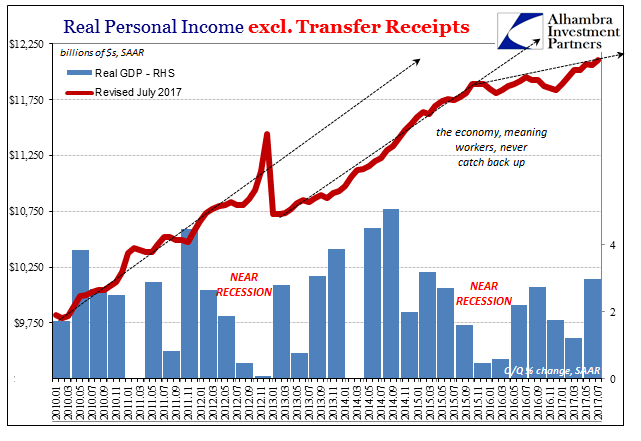

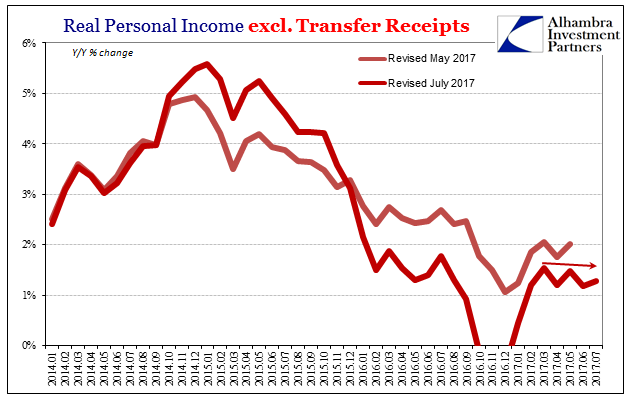

Proving Q2 GDP The Anomaly, Incomes Yet Again Fail To Accelerate5 Sep 2017

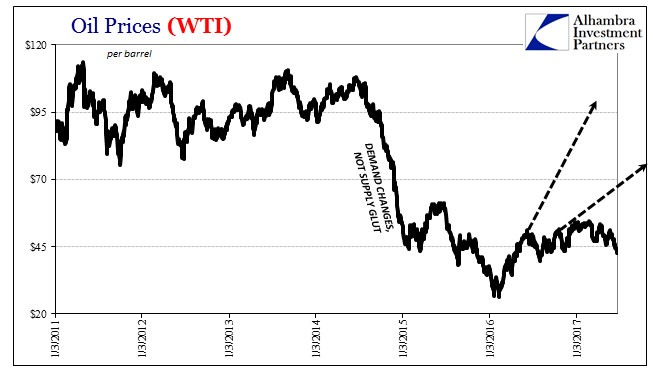

Oil Prices and Manufacturing PMI: No Backing Sentiment4 Jul 2017

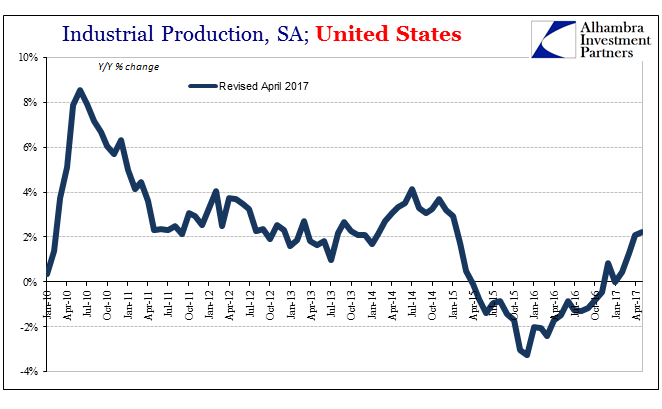

Defying Labels25 Jun 2017