Read More »

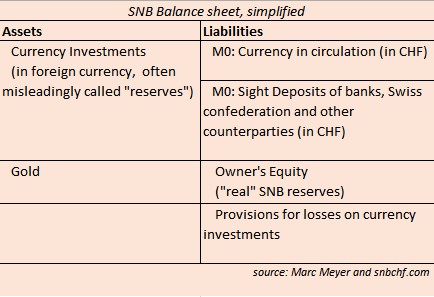

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

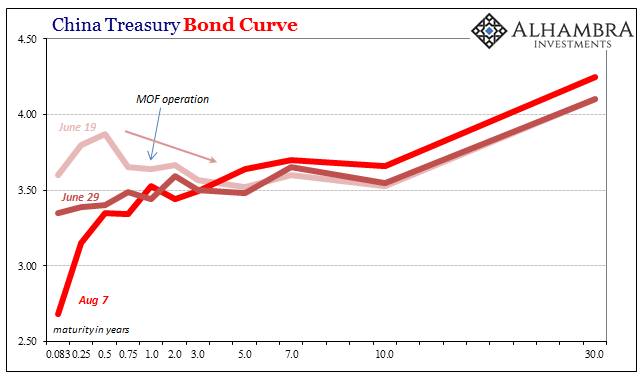

China and the US at sovereign debt war

China and the US at sovereign debt war27 Jan 2023

They’ve Gone Too Far (or have they?)10 Jan 2021

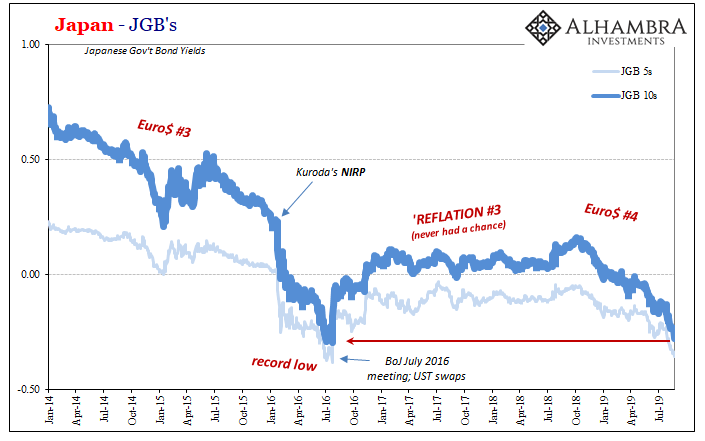

Why The Japanese Are Suddenly Messing With YCC6 Oct 2019

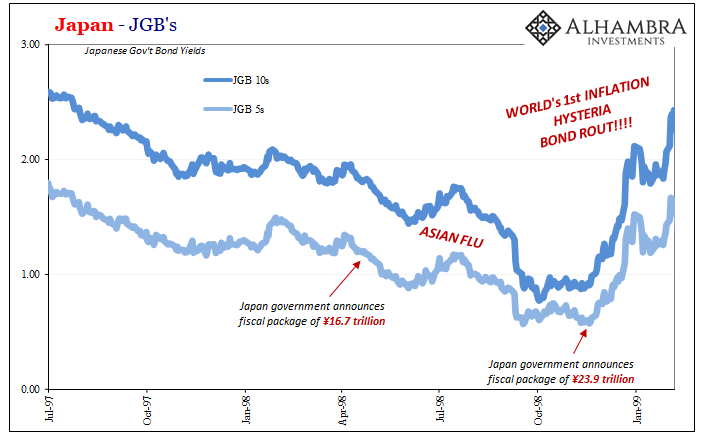

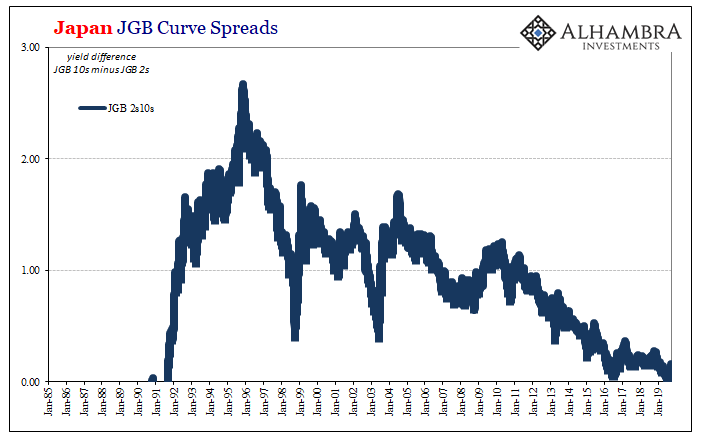

Japan: Fall Like Germany, Or Give Hope To The Rest of the World?29 Aug 2019

Bonds And Soft Chinese Data4 Nov 2017

Systemic Depression Is A Clear Choice5 Apr 2017

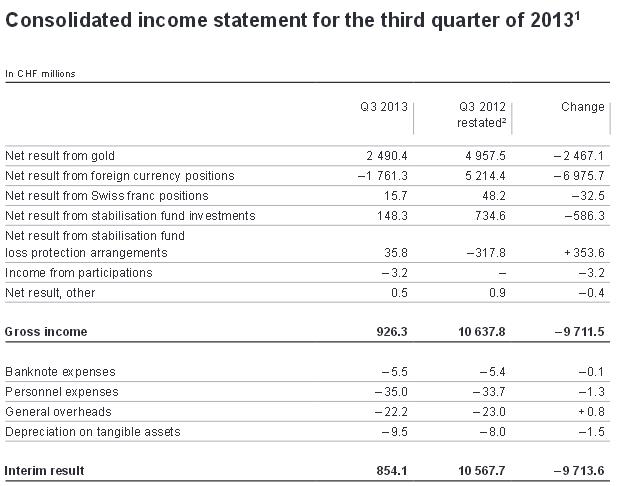

In Which Positions Does the SNB Win and Where Does it Lose Money: Details on the Q3 Results30 Oct 2013

SNB Q2/2013 Composition of Reserves2 Aug 2013

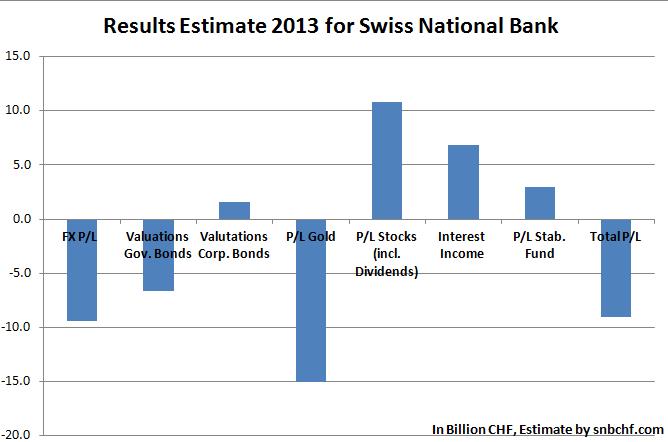

Our Detailed Estimate of SNB Q2 Results: 17 Billion Francs Loss, The Reality 18 Billion30 Jul 2013

SNB Q1 Results: Bottom-Fishing Cheap Yen, Increases Equity Share with Gains and Margin Debt30 Apr 2013

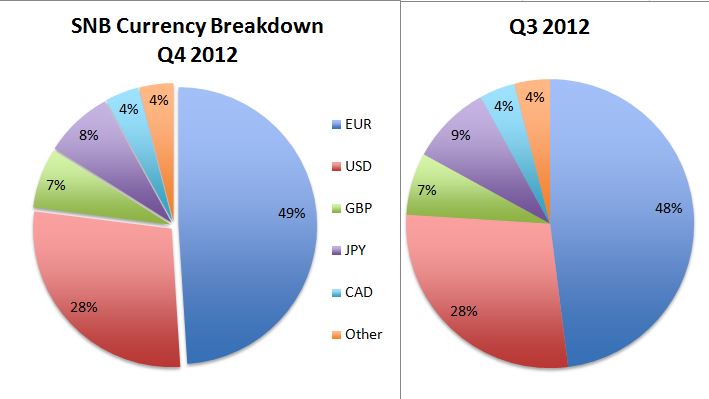

Composition of SNB Reserves Q4, 2012, Yield on Investment7 Mar 2013

Trade Like a Central Bank: Buy EUR/USD at 1.24 and sell at 1.30! .. SNB31 Oct 2012

Did the SNB Front-Run ECB Decisions Far Ahead of Hedge Funds?30 Oct 2012

Is Standard and Poor’s a Rating Agency or a Rumor Agency ?1 Oct 2012

Are German Bunds finally heading for the big slide ?14 Sep 2012

German Schatz turns negative again

German Schatz turns negative again18 Jul 2012

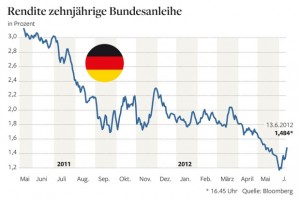

The other risk for the SNB: Will German Bund yields double ?

The other risk for the SNB: Will German Bund yields double ?20 Jun 2012

The Northern Euro introduction: A retrospective from the year 2030

The Northern Euro introduction: A retrospective from the year 203020 May 2012

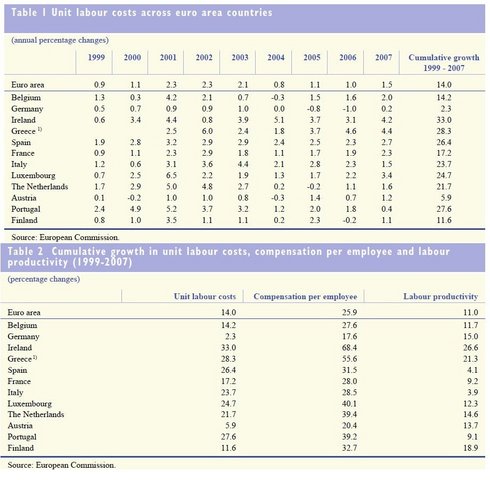

Jürgen Stark’s resignation and the ECB 2005 warning about labor cost divergence in the Euro-zone

Jürgen Stark’s resignation and the ECB 2005 warning about labor cost divergence in the Euro-zone18 Dec 2011

China and the US at sovereign debt war

2023-01-27

by Stephen Flood

2023-01-27

Read More »