Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Will the Market Push the Dollar Above JPY152 as Japanese Prime Minister Heads to the US?

Will the Market Push the Dollar Above JPY152 as Japanese Prime Minister Heads to the US?8 Apr 2024

Sterling Buoyed by Labor Market Report Ahead of US CPI13 Feb 2024

The Greenback is in Narrow Ranges to Start the Week12 Feb 2024

Greenback Consolidates Two-Day Surge6 Feb 2024

Greenback Surges as Rates Back Up16 Jan 2024

Consolidation Featured8 Jan 2024

Consolidative Tone Emerges Ahead of Tomorrow’s US Jobs and EMU CPI4 Jan 2024

Canadian Dollar Plays A Little Catch-Up, Rises to best Level in Nearly Seven Weeks28 Nov 2023

Dollar Consolidates Amid Rate Volatility16 Nov 2023

US CPI Front and Center, but Can Congress Avert a Government Shutdown?14 Nov 2023

Food Prices Drive China’s CPI Lower while the Greenback is Mostly Firmer in Narrow Ranges9 Nov 2023

The Dollar’s Recovery has been Extended, but it may Give North American Operators a Better Selling Opportunity7 Nov 2023

DZ BANK startet eigene Crypto Verwahrung3 Nov 2023

Divergence Continues to Underpin the Greenback25 Oct 2023

Markets Remain on Edge17 Oct 2023

Bonds Extend Recovery

Bonds Extend Recovery11 Oct 2023

War in Israel Spurs Flight to Dollars, Yen and Gold, While Driving up the Price of Oil9 Oct 2023

US Employment Data to Determine Whether the Greenback’s Rally since mid-July is Over…Maybe6 Oct 2023

Looming US Government Shutdown Stems the Dollar’s Surge28 Sep 2023

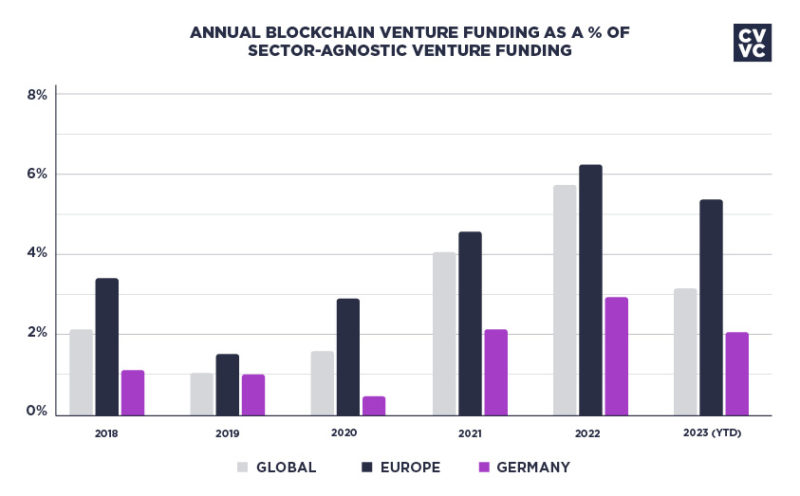

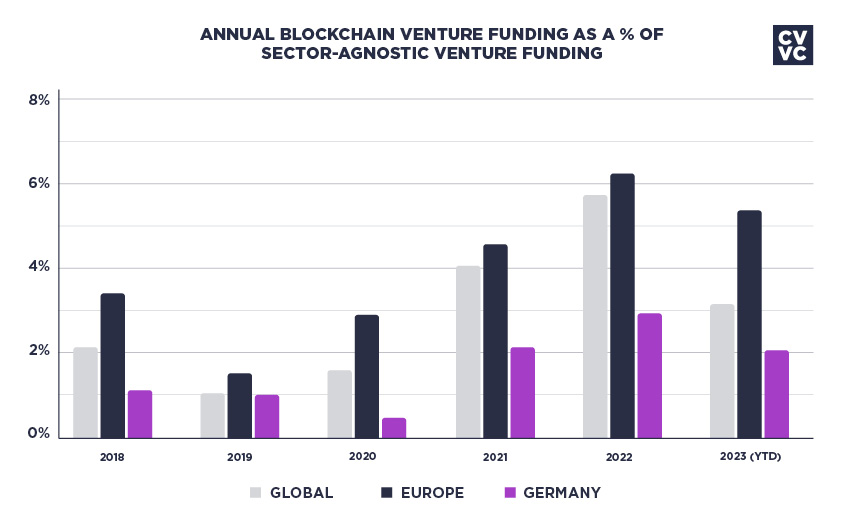

Funding Overview Blockchain Germany 2023

Funding Overview Blockchain Germany 202320 Sep 2023