Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

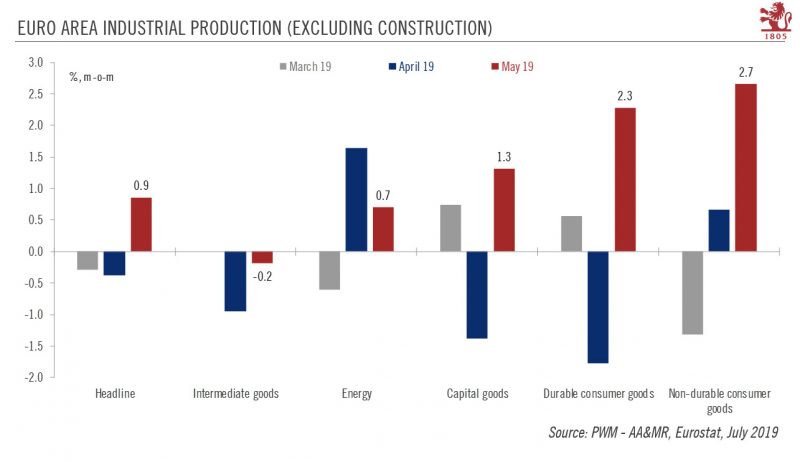

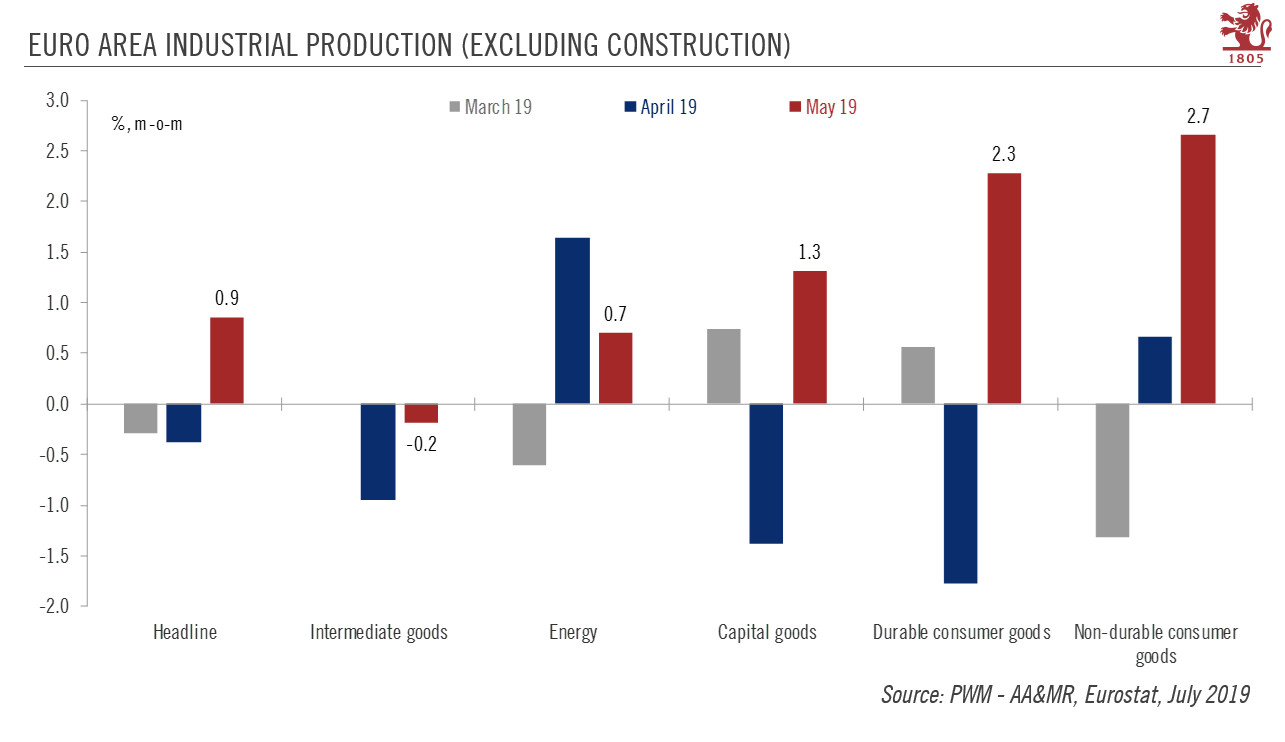

Euro area manufacturing is not out of the woods

Euro area manufacturing is not out of the woods19 Jul 2019

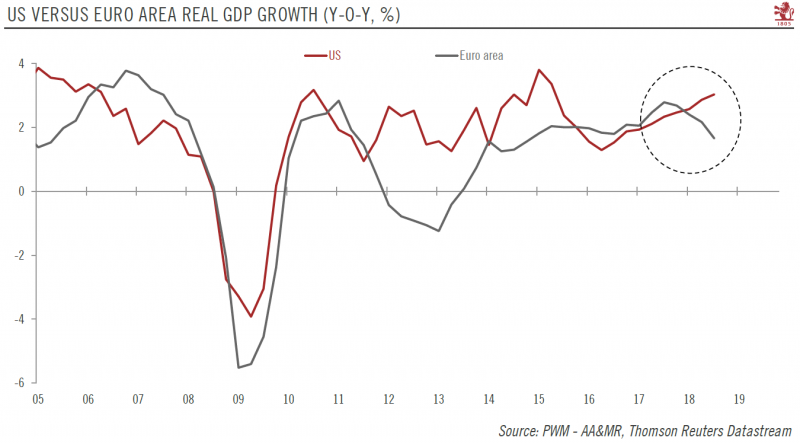

Rising downside risks to euro area growth23 May 2019

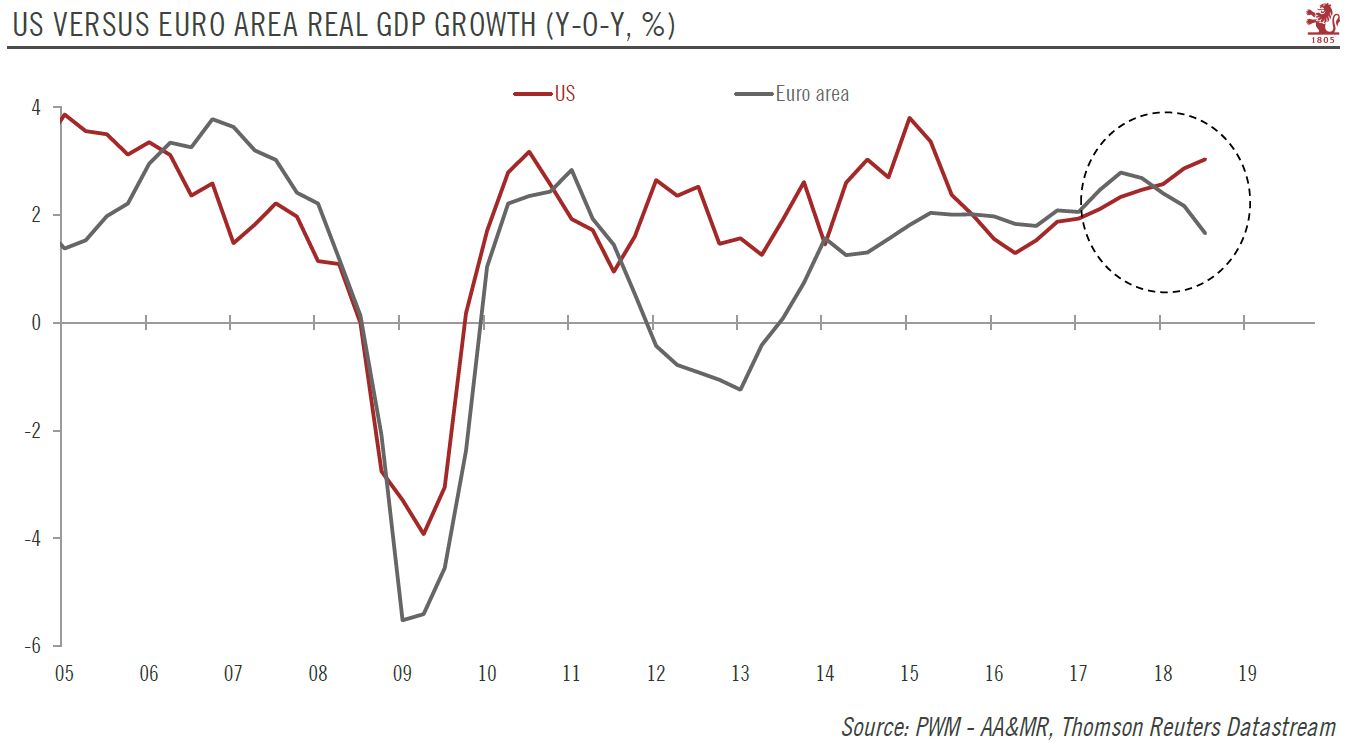

Euro area’s initial growth figures for Q3 prove disappointing

Euro area’s initial growth figures for Q3 prove disappointing31 Oct 2018

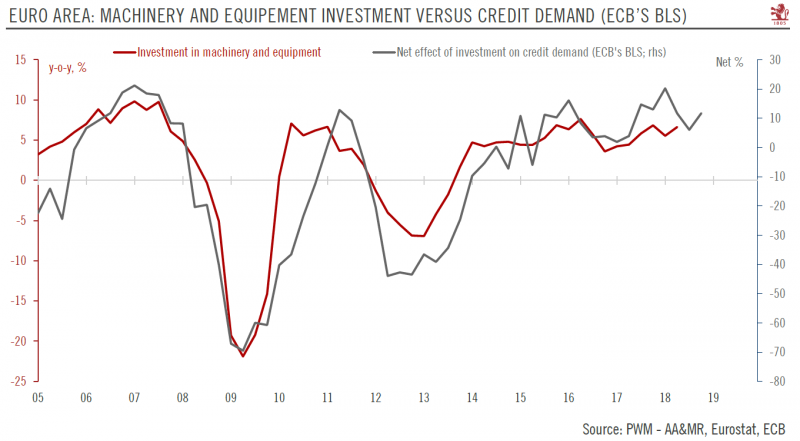

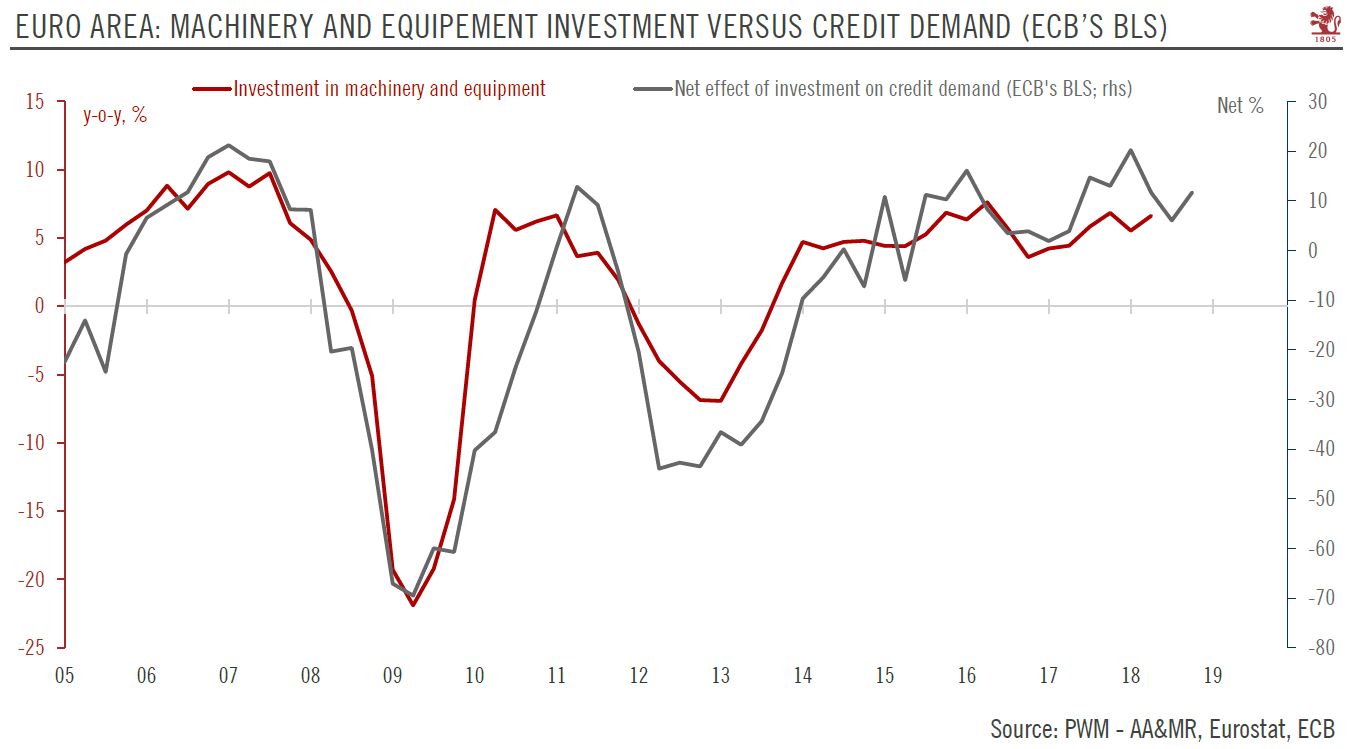

Credit Conditions in the Euro Area Remain Supportive of Investment Recovery

Credit Conditions in the Euro Area Remain Supportive of Investment Recovery29 Oct 2018

Gloomy Signals for Euro Area Manufacturing

Gloomy Signals for Euro Area Manufacturing25 Oct 2018

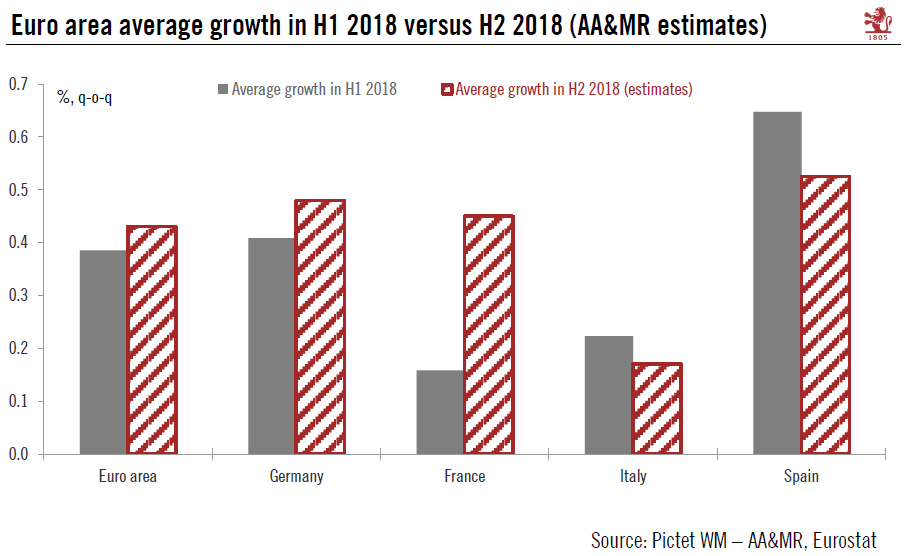

Contrasting Fortunes within the Euro Area

Contrasting Fortunes within the Euro Area21 Sep 2018

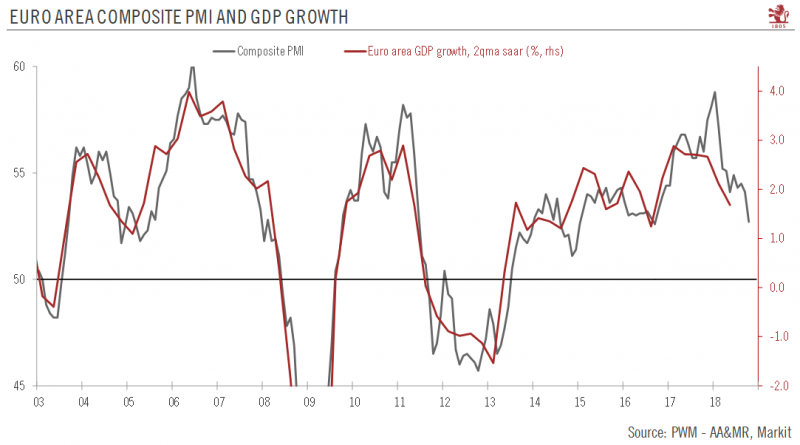

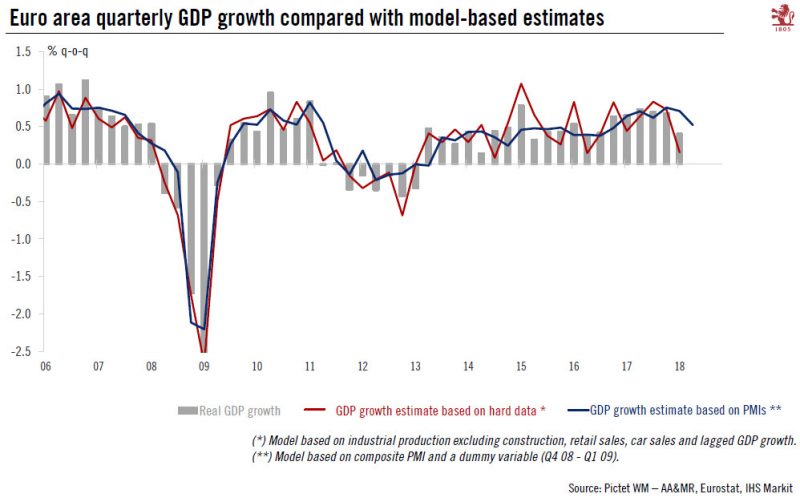

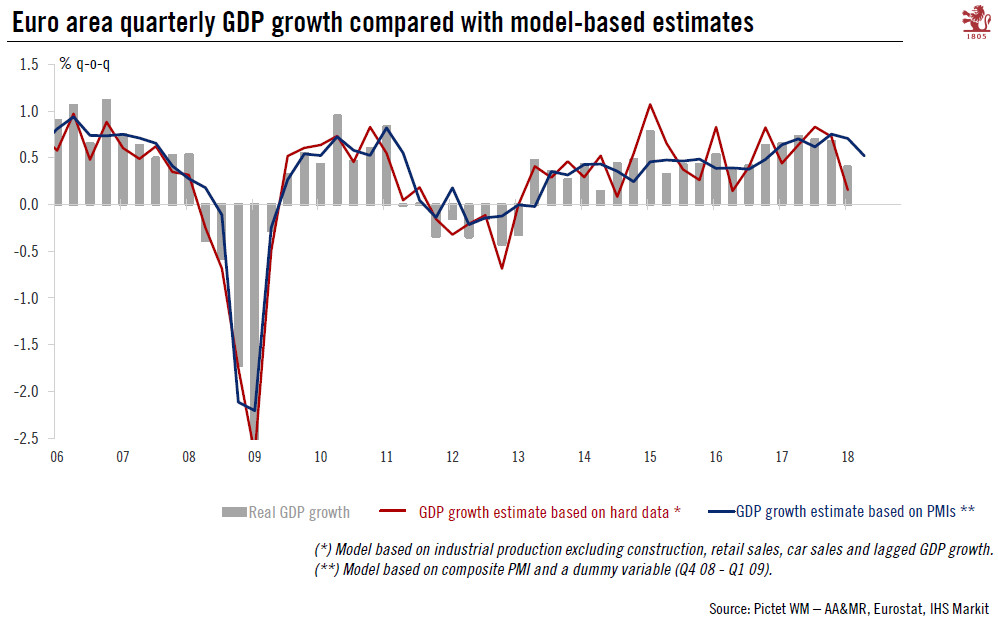

PMIs point to downside risk to near term euro area growth

PMIs point to downside risk to near term euro area growth24 May 2018

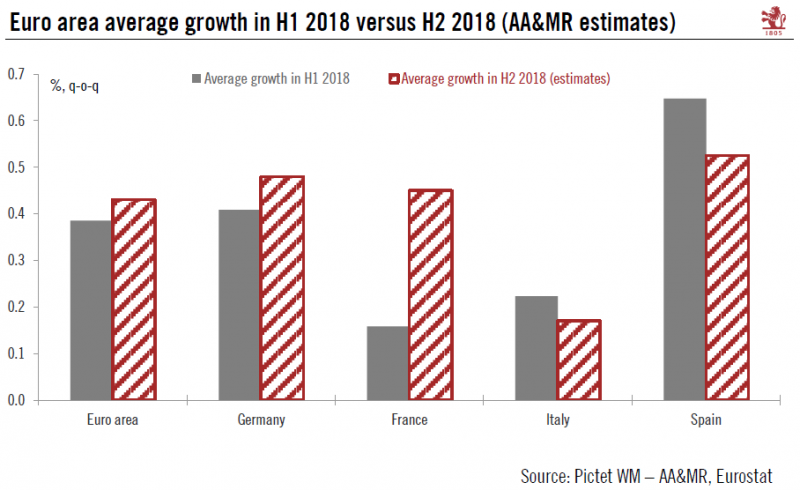

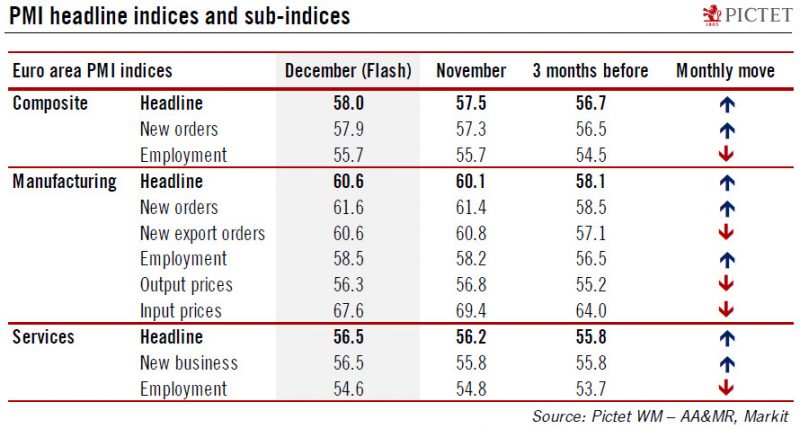

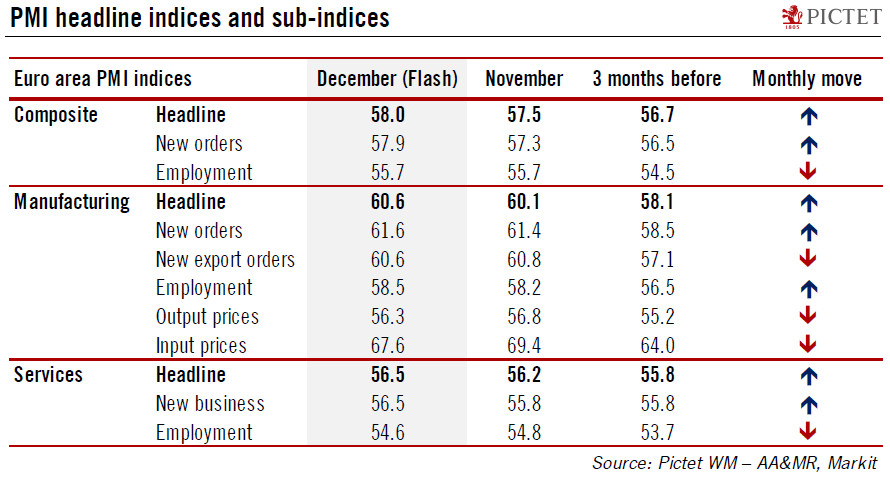

Euro area: The sky is the limit

Euro area: The sky is the limit20 Dec 2017