Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

GDP + GFC = Fragile

GDP + GFC = Fragile1 May 2020

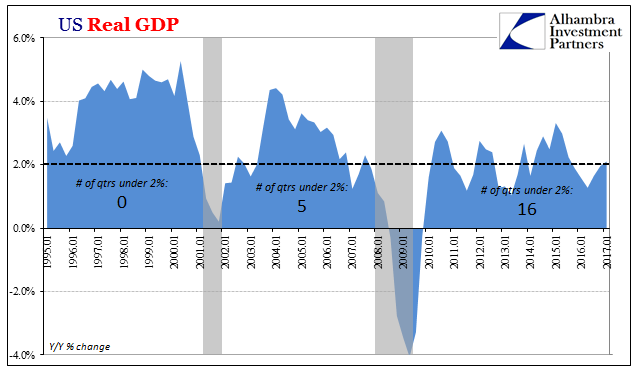

Three Straight Quarters of 2 percent, And Yet Each One Very Different2 Feb 2020

Consistent Trade War Inconsistency Hides The Consistent Trend5 Dec 2019

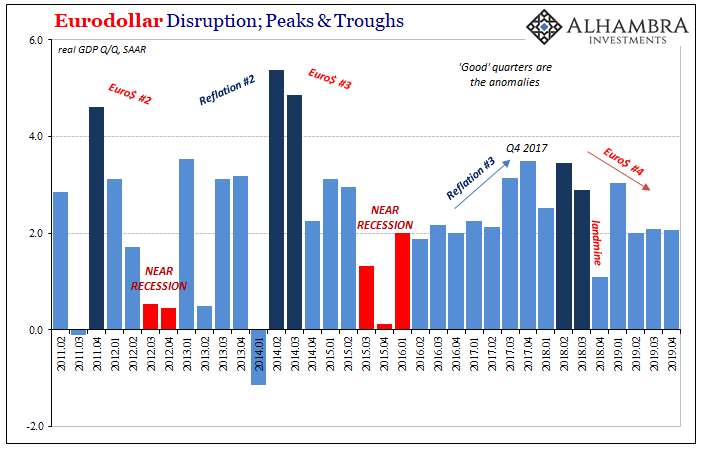

Three (Rate Cuts) And GDP, Where (How) Does It End?1 Nov 2019

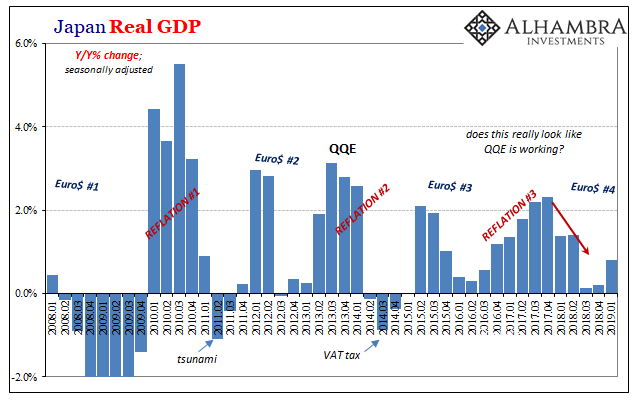

Japan’s Surprise Positive Is A Huge Minus21 May 2019

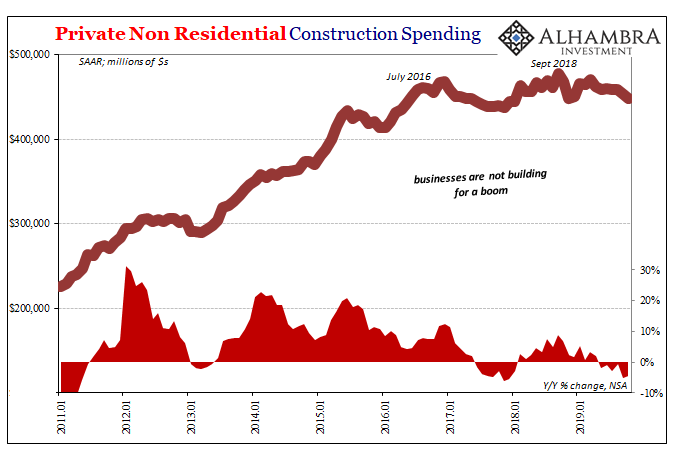

Now Capex?9 Sep 2017

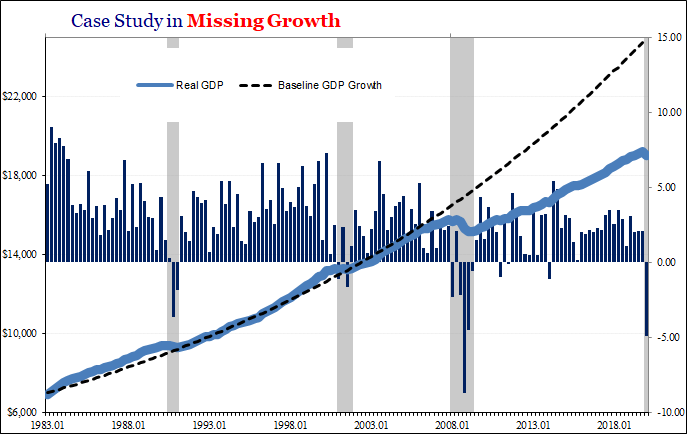

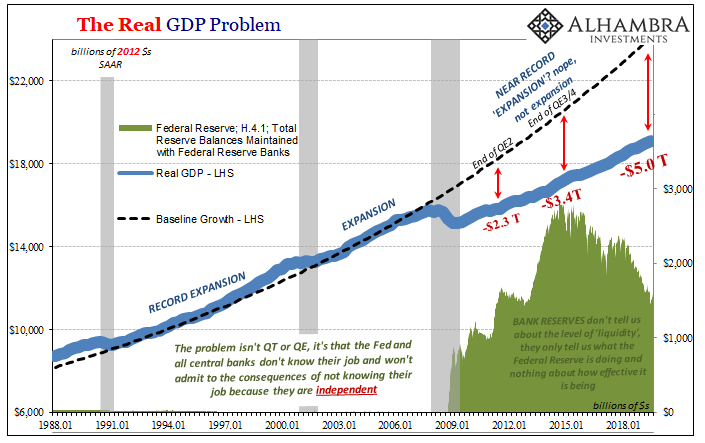

U.S. Gross Domestic Products: Near Record Expansion (Really Reduction)7 Jul 2017

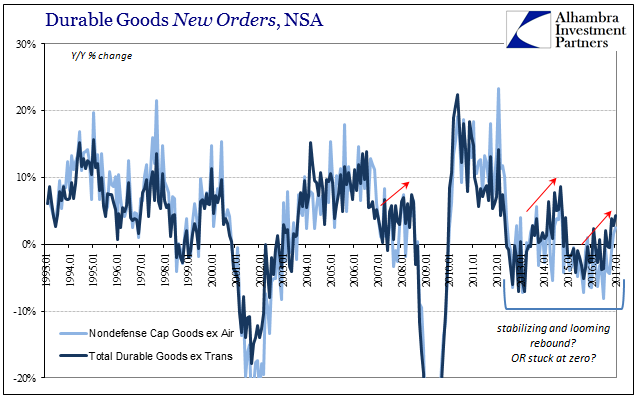

Durable Goods Groundhog28 Feb 2017

No Acceleration In Industry, Either20 Feb 2017