Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

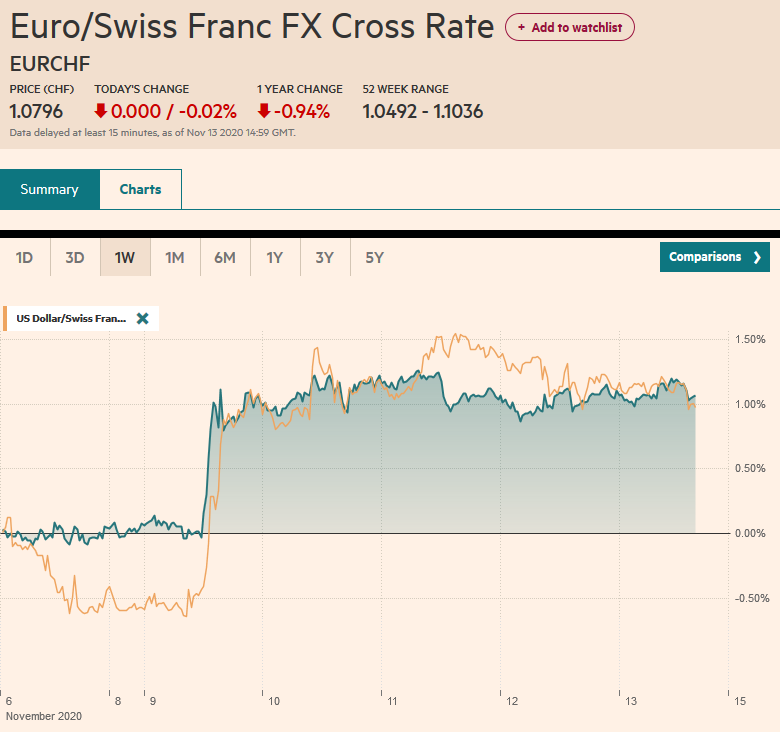

Swiss FrancThe Euro has fallen by 0.02% to 1.0796 |

EUR/CHF and USD/CHF, November 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

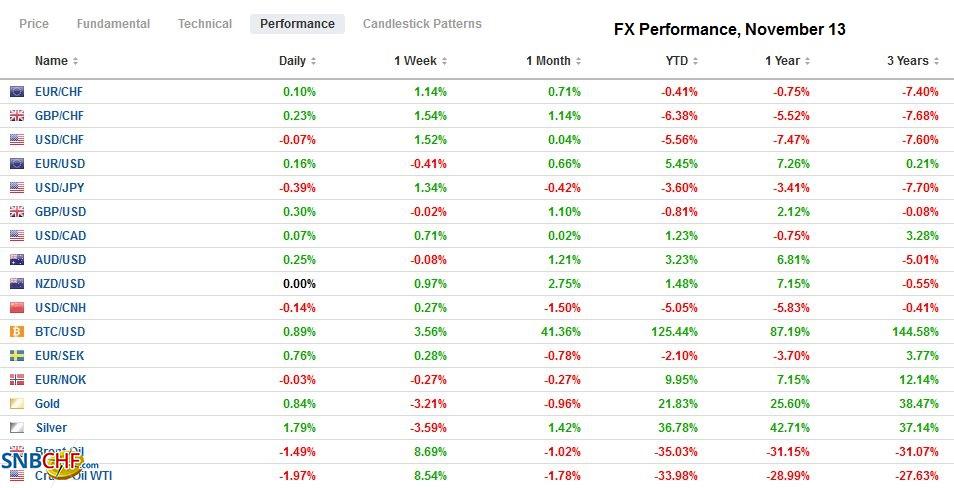

FX RatesOverview: The largest bourses in the Asia Pacific region followed the US equity market lower, with the Nikkei posting its first loss in nine sessions. China, Hong Kong, and Australia moved lower as well. On the week, the MSCI Asia Pacific Index gained about 1% after rising 6.3% in the prior week. China’s markets are the only ones in the region not to move higher this week. European shares are little changed today and are up a little more than 5% this week after gaining 7% in the previous week. US shares are firm. The S&P 500 brings a 0.8% gain this week into today’s session. It was up 7.3% last week. The US 10-year Treasury yield of 0.88% is off four basis points this week, though steady today. European yields are a little softer today, and on the week, the core yields are off 3-4 bp, while the peripheral yields are off 4-8 bp. Of note, here too, China is moving in the opposite direction. Its benchmark 10-year yields rose three basis points this week to 3.25%. The dollar is mostly softer, but it is higher against all the major currencies this week, save the New Zealand dollar, where the market has unwound the likelihood of negative policy rates. Among emerging markets, the Turkish lira surged nearly 11.5% this week, as the new economics team and a perhaps chastened president spurred the dramatic short-covering rally. The JP Morgan Emerging Market Index is up about 0.5% this week after last week’s 2.5% gain. Gold is hovering around $1880, off about 3.7% this week, and effectively giving back last week’s gains to be little changed here in November. Crude oil is softer on the day, but the December WTI is still up about 9.5% this week after rising 3.8% last week. It is near $40.70 and settled October a little above $37. |

FX Performance, November 13 - Click to enlarge |

Asia Pacific

The G20 meeting of finance minister and central bankers is to further progress on debt relief for the poorest countries. The measure of success is if China, which is the official largest creditor and is owed almost two-thirds of the debt payments this year by the poorest countries. After agreeing in principle to a framework last month, the hope is that China accepts a similar approach as the Paris Club (of creditor nations). The G20 seeks a standardized approach.

A combination of large money market operations maturing and speculation that the PBOC will begin unwinding emergency measures has roiled China’s money market this week that had sent the overnight repo to its higher levels since January. Rates eased today after officials said that they would inject CNY160 bln into the banking system, the most since late September. On Monday, the PBOC will inject funds via the Medium-Term Lending Facility (MLF). Large operations are rolling off this month, and the size of the PBOC operation will shed light on Beijing’s intent.

By executive order, the US prohibited investment in 20 Chinese firms controlled by the Chinese military. This seemed to weigh on the shares of the impacted companies today, but the entire market was heavy, as we noted. Separately, pending the judicial process, TikTok has been given a reprieve from being banned in the US.

The dollar slipped to a three-day low near JPY104.85 today, but it continues to consolidate Monday’s surge that lifted it from around JPY103.20 to a high near JPY105.65. A marginal new high was made in the middle of the week, but a consolidative tone has persisted. Support is seen near JPY104.75, which houses a $390 mln option that expires today. On the upside, the JPY105.30-JPY105.40 offers resistance. The Australian dollar made a marginal new low for the week close to $0.7220 today but has been bid up to $0.7260 in the European morning as its little changed on the week. Nearby resistance is around $0.7280 and then $0.7300, where nearly A$600 mln option rolls off today. The PBOC set the dollar’s reference rate at CNY6.6285 in line with projections. The dollar is virtually flat against the yuan this week. The yuan has risen in all but four weeks here in H2 20.

EuropeOne would not know it looking at sterling, which with today’s gain now around 0.4% is higher on the week, that the UK-EU trade talks have shown little progress as the next deadline, mid-November is at hand, the Bank of England projects a 2% contraction this quarter, the virus appears rampant, and Prime Minister Johnson has lost two close advisers. In the middle of the week, the Communications Director tipped to be the next Chief of Staff unexpectedly resigned. |

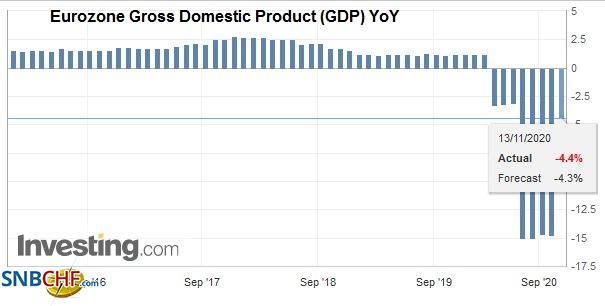

Eurozone Gross Domestic Product (GDP) YoY, Q3 2020(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| Yesterday it was confirmed that Cummings will also leave the government before the end of the year. The timing could not be worse for Johnson. Separately, while the risk of a negative base rate appears to have diminished, the Sunak, the Chancellor of the Exchequer, is working on another round of fiscal stimulus. |

Eurozone Employment Change YoY, November 2020(see more posts on Eurozone Employment Change, ) Source: investing.com - Click to enlarge |

The EU’s 1.8 trillion euro budget includes the 750 bln euro Recovery Fund passed important hurdles at the EC and the European Parliament. However, the toughest challenge still lies ahead. The Recovery Fund was heralded in some quarters as a Hamiltonian Moment. Even those not so enthralled, saw it as important. We suggested it was like scaffolding for the evolving European Project but recognized that the fight about the fiscal union was for another day. Still, rather than make its emergency assistance, the EU has turned it into a cudgel to enforce Brussels values and links assistance to adherence to the rule of law. This is specifically aimed at Hungary and Poland. The EU budget requires unanimity, and today Poland’s Prime Minister Morawwiecki has joined Hungary’s Orban in threatening to veto the budget. This could trigger a new European crisis and is taking place at the same time the UK-EU trade talk deadline.

The euro is firm but well off the $1.1920 high seen on Monday. Since then, it has been encountering resistance in the $1.1830-$1.1840 area. It tested that resistance in the European morning and found sellers have not been satiated. There is an option for 1 bln euro at $1.18 and another for about 715 mln euros at $1.1850 that expire today. Recall that the euro finished last month a little below $1.1650. Sterling fell by almost 0.8% yesterday and has recovered more than half today to trade near $1.3185 in the European morning. It held just above $1.31 in Asia, where a GBP320 mln option expires later today. Resistance is seen in the $1.3200-$1.3220 area.

America

The US Senate may vote next week on two Fed appointments. The first, Waller, the director of research at the St. Louis Fed, is hardly controversial. The second is a different issue. Shelton’s views on gold, on deposit insurance, and on the Federal Reserve itself appear far outside the spectrum of views associated policymakers. The Republicans have a 53-47 majority in the existing Senate. Two Republicans (Romney and Collins) have said they cannot support Shelton’s candidacy.

The US reports October PPI today, and it is typically not a market-mover. Still, a 0.2% increase in the headline and core rates will leave the year-over-year measures unchanged at 0.4% and 1.2%, respectively. The University of Michigan’s preliminary November confidence readings will draw some attention in light of the virus’s surge and new social restrictions. The inflation survey may also be watched. The 1-year expectation was at 2.6% in October, and the 5-10 year view was 2.4%.

Mexico surprised many yesterday when the central bank left its overnight target at 4.25%. More than two-thirds of the economists polled by Bloomberg expected a 25 bp cut. The vote at Banxico was 4-1 in favor of a steady policy. Inflation has doubled since April and has been above the upper end of the 2-4% target range for three months. The economy may contract by 10% this year, and President AMLO is reluctant to draft a large fiscal stimulus, and monetary policy is the only lever. Food prices are a major driver of Mexico’s inflation and the price pressures being experienced by other emerging market economies. Private-sector economists expect CPI to pullback next year. Separately, in response to news that its inflation jumped 3.8% in October for a 37.2% year-over-year rate, Argentina’s central bank immediately hiked rates, including a 200 bp increase in the Leliq to 38%, and hike the repo rate on retail CDs.

The US dollar fell to new lows for the year against the Canadian dollar to start the week (~CAD1.2930) but rebounded smartly to CAD1.3170 earlier today. The greenback has been turned lower and tested the CAD1.3115 area in the European morning. An option for around $825 mln at CAD1.3125 will be cut today. Initial support is seen near CAD1.3080. The Mexican peso briefly strengthened on the central bank’s surprise standpat decision, but then it was sold to new session lows. Today, the US dollar set the high for the week near MXN20.69. Support is seen around yesterday’s low (~MXN20.43).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Currency Movement,EU,Featured,Mexico,newsletter,U.K.