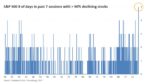

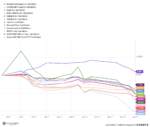

So, is that it? Have rates peaked? Is the long bear market finally over?

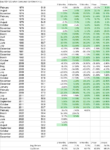

The market decided last week that interest rates have peaked for this cycle. And if rates have peaked then all the assets that have been pressured over the last two years can finally come up for air. Since October 18, 2021, over two years ago, investors have had few places to hide. Of the major asset classes we follow closely, only two – gold and commodities – were higher by more than a rounding error over that time.

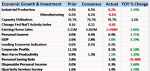

The culprit, the reason stocks and bonds did so poorly over that time, is pretty simple – interest rates. The 10-year Treasury note yield roughly tripled during that time and all assets have been affected by those higher rates. Since January 1. 2021, the consumer price index has risen by 17.5%, a 6%

Read More »